A Play, a Subtitle, and Four Hundred Years of English Greed

I. Begin with the Subtitle

Caryl Churchill called her play a city comedy. She put it right there in the subtitle, in case anyone missed it: Serious Money: A City Comedy. This is not a casual generic label. It is a provocation, a genealogy, and a structural argument compressed into two words. She is telling her audience — all of her audiences, the left-cultural crowd at the Royal Court and the traders who followed them at the Wyndham’s — that what they are watching is not new. It has happened before. In 1605 Ben Jonson wrote Volpone, a play about a Venetian magnifico who feigns terminal illness to extract gifts from legacy hunters. In 1610 he wrote The Alchemist, a play about an empty house, three con artists, and an inexhaustible queue of Londoners willing to be parted from their money in exchange for the promise of impossible returns. In 1692 Thomas Shadwell wrote The Volunteers, or The Stockjobbers, which Churchill opens her play with, a scene about investors discussing whether the actual utility of a patent matters at all, and arriving at the obvious answer: it doesn’t, as long as you can generate enthusiasm for the stock.

The date on Shadwell’s play is worth holding. 1692. And it is not merely a convenient genealogical reference. Shadwell was writing in real time about an actual market crisis — the stock market bubble of 1692, England’s first speculative mania, not dissimilar in character to the South Sea Bubble that would follow within a generation. Churchill knew this. She is not drawing an analogy between 1692 and 1987. She is demonstrating that the same event has happened repeatedly, that the participants each time believed they were in a new world, and that the interval between bubbles is simply the time required for institutional memory to fail and a new generation of clever, hungry people to arrive at the trading floor. Within a century of Shadwell, the canal mania and the railway mania would demonstrate that the English had learned nothing except how to lose larger sums more efficiently. Within three centuries, a deregulation event called Big Bang would remake the City of London overnight, and a playwright who had been collecting newspaper cuttings in scrapbooks would write a play about it within five months, in rhyming couplets, with songs by Ian Dury, and she would be right about everything.

Churchill also makes a surgical editorial decision with the Shadwell extract. A character named Nickum, who draws attention to the ‘stock-jobbing rogues’ and provides the one voice of explicit criticism in the original, has been excised. With Nickum gone, there is no critical conscience in the scene. The greed proceeds without commentary. This is Churchill’s argument in miniature, enacted through an act of editing before the play proper has begun.

This essay is about that play. It is also about the genre it inhabits and extends, about the audience that cheered it and the audience that couldn’t follow it and the audience of traders who cheered it for reasons Churchill may not have fully intended. It is about what the play understood that the critics didn’t, and what the play couldn’t say that the decades since have made visible. It is about Caryl Churchill, who stopped giving interviews many years ago and lets the plays do the talking, which is itself a politics. And it is about what it means to write a socialist feminist satirical city comedy in the same year as Black Monday, in a country that had just re-elected the government it was supposed to be satirising, and have the people you are satirising buy the tickets and leave happy.

The answer to that last question is complicated. Let us start with the history.

II. The World the Play Walks Into

On 27 October 1986 — a single overnight moment — the London Stock Exchange was deregulated. The event had a name, Big Bang, that was entirely appropriate: something compressed and unstable released its energy all at once, and the landscape it occupied was permanently altered. Fixed commissions were abolished. The separation between jobbers (who held stock) and brokers (who dealt with clients) was ended. Foreign ownership of British firms was permitted. Electronic trading replaced the face-to-face system. American and European banks poured in.

The popular account of Big Bang focused on the visible theatre of it: the Essex boys replacing the toffs, open-outcry replaced by screens, blokes shouting in coloured jackets giving way to people in silence staring at terminals. In the play this is Grimes replacing Frosby, and it is real. But it understates what actually happened. The deeper transformation was the admission of foreign capital — American and European banks acquiring British firms, the City becoming a node in a global financial network rather than a national institution with gentlemanly pretensions. The London Stock Exchange was in effect privatised, repriced below global competitors, opened to flows of capital that had previously been excluded. London’s position had already been consolidated through the Eurodollar market — the offshore dollar market that had grown in the 1960s and 70s, largely unregulated, largely in London — and Big Bang extended that logic into equities and other markets. This is David Harvey‘s compression of time and space made institutional: capital moving faster, further, with fewer obstacles, accumulating value across distances and time horizons that had previously been unavailable to it.

What Big Bang actually did was replace one form of credentialism with another while leaving the fundamental extraction unchanged. The old City ran on class: public school, university, the right club, the right accent, the word of a gentleman being sufficient bond because gentlemen were the only people in the room. The new City ran on education and technical competence — the ability to price a derivative, to rapidly digest everything on a screen, to think faster and smarter than the person opposite. Salaries exploded. Young men and, for the first time in significant numbers, young women, found themselves earning in a month what their parents earned in a year. The LIFFE — established in 1982, already operating its open-outcry floor of hand signals, shouting, and physical performance — accelerated sharply as Big Bang brought new capital and new participants into its world. The performance space was pre-existing. Big Bang filled it further.

The City had always attracted a certain personality type, but Big Bang concentrated and accelerated it. What drove these people was not, in most cases, simple avarice — though avarice was certainly available. What drove them was the game. The money was the scorecard. You were right about the trade or you were wrong, and the number told you which, and the number updated in real time, and the next trade was already opening before the last one closed. It was, and remains, pharmacologically indistinguishable from gambling: the action, the dopamine hit of the win, the belonging to a tribe of people who understand that this is what life is actually for. Tom Wolfe called them Masters of the Universe. The phrase was ironic. They took it as a compliment. They were not wrong to.

Outside the City, in the Britain of 1986-87, things were different. Unemployment was falling from the catastrophic highs of the early Thatcher years but remained stubbornly elevated. The coal industry had been broken. Manufacturing had contracted. The NHS was under pressure. But the government had been re-elected in 1983 with a landslide, and would be re-elected again in 1987 with another. The political settlement was Thatcherism — the market as the answer to all questions, greed rebranded as rational self-interest, the state’s job to get out of the way and let the invisible hand do its work.

Also in November 1986: Ivan Boesky was charged with insider trading in New York and paid $100 million to settle. He had, earlier that year, told the graduating class of the University of California Business School that greed is healthy. He was not the first person to think this. He was perhaps the first person to say it quite so baldly in front of an audience that applauded.

Churchill opened her scrapbooks and began to write. She had spent weeks on the LIFFE floor and in dealing rooms with director Max Stafford-Clark and the company. The traders, she said, ‘were very helpful.’ The attraction and repulsion of financial markets — the energy, the immorality, the sheer theatre of the thing — is present in the play and the audience reactions confirmed it. Churchill did not step away from the fascination. She put it in.

She started writing after Christmas 1986. The rehearsal draft was complete by 15th February 1987. Seven weeks of actual writing. On the day of the first read-through, Max Stafford-Clark was meeting Margaret Thatcher to discuss arts subsidies. Tory policy was that market logic should extend to the arts — theatre should seek corporate sponsors, reduce its dependence on public funding. The first read-through of a play about the consequences of exactly this logic happened on the same day its director sat down with its chief architect. Churchill could not have planned it. She didn’t need to.

III. The Playwright and the Silence

Caryl Churchill was born in London in 1938, the only child of a political cartoonist and a model. She spent her childhood in Montreal, returned to Oxford, wrote plays at university, married a barrister called David Harter, had three sons, wrote radio plays for the BBC through the 1960s while raising a family, and then — in the mid-1970s, slowly and subjectively, as she later described it — became a feminist. She had been a writer first. The feminism arrived through her own experience rather than through political events, which may be why it went so deep and so structural.

Her career from that point describes a consistent arc: the collaborative workshop process with Joint Stock and Monstrous Regiment, then the long partnership with Max Stafford-Clark at the Royal Court — Cloud Nine (1979), Top Girls (1982), Fen (1983), Serious Money (1987). She won Obie after Obie. She collected the Olivier. The critical establishment decided she was one of the major British dramatists of the twentieth century.

She stopped giving interviews. She has been publicly silent for decades. She rarely comments on analyses of her work. There are no profiles, no podcasts, no explanatory essays. The plays speak. She does not.

This silence is worth dwelling on because it is consistent with her politics rather than in tension with them. The playwright who becomes a public intellectual — who explains their work, contextualises it, makes themselves available to be interviewed and photographed and asked their opinions — is participating in the celebrity economy that her plays consistently anatomise. The author as brand. The artist as content. Churchill declines. This is not false modesty. It is a politics of form applied to a career, and it extends to her practice: she does not write to commission, she retains her rights, she specified Stafford-Clark as director for the American transfer. The work moves on her terms or not at all.

The practical consequences for directors and actors are significant and underacknowledged. Churchill’s published texts carry almost no stage directions. Where Beckett is tyrannically precise and Shaw’s directions are essentially essays, Churchill gives you the words and the speakers and leaves everything else open. This is not laziness or oversight. It is the same politics as the public silence: the play does not explain itself, does not pre-interpret its own meaning. The director must be a co-author, which is why the pool of directors who take her on remains small — Stafford-Clark, Stephen Daldry, James Macdonald, Lyndsey Turner — and why productions of her work that get the register wrong tend to fail catastrophically rather than merely disappointingly. The absence of instruction is itself an instruction, and reading it correctly requires exceptional theatrical intelligence.

What we know of her views comes from the plays themselves and from a handful of early interviews. Her utopian aspiration, stated once: a society that is decentralised, non-authoritarian, communist, non-sexist — a society in which people can be in touch with their feelings and in control of their lives. The positive that Serious Money’s negative implies throughout. She is not an optimist about whether this society is achievable. She is entirely clear that the society she actually lives in is its opposite.

Her father drew political cartoons: images compressed to a single visual argument, satirical, exaggerated, designed to make a point that extended prose could not. This formal inheritance is not incidental to Serious Money. The play is, among other things, a series of political cartoons animated and put onstage. The characters are not psychologically rounded. They are not meant to be. They are drawn with the concentrated venom of a caricaturist, and the couplets are the speech bubbles. There is a lineage from Jacobean City Comedy to Shadwell to the satire of Swift, the political cartoons of Hogarth and then Gillray and Rowlandson to broadside and music hall and on to her father. Churchill used this inheritance and, in Ian Drury, found a collaborator for the songs in the play who was also well versed in the tradition.

IV. What Kind of Object Is This?

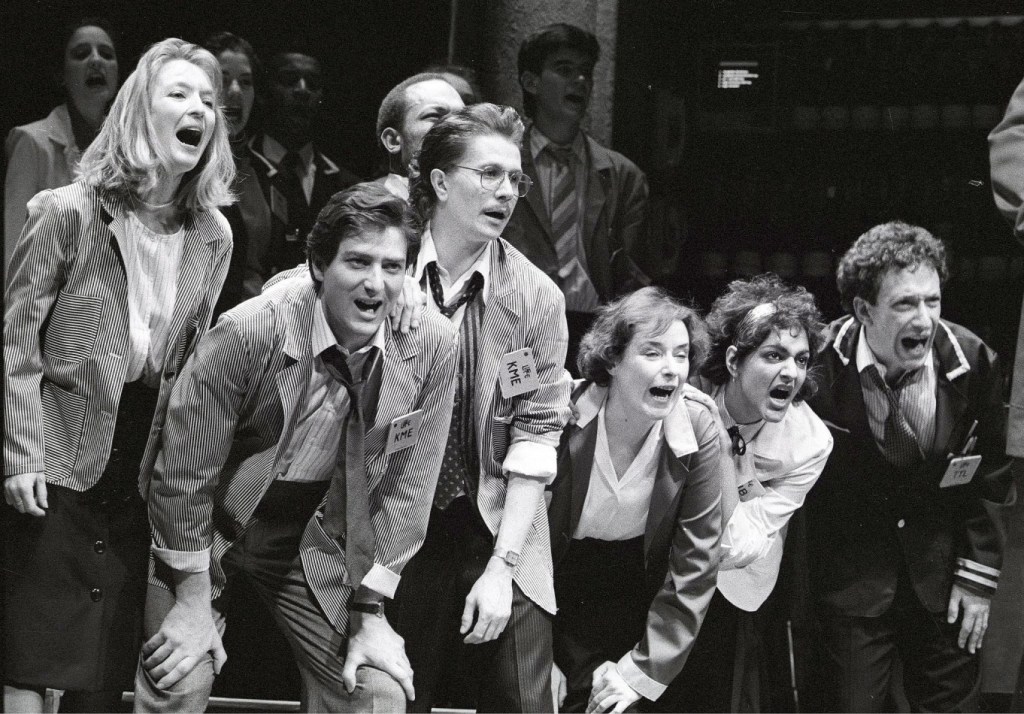

The play was developed at the Royal Court through the workshop process that Churchill and Stafford-Clark had refined together over a decade. The technical vocabulary — greenmail, white knight, arbitrageur, stale bull, concert party, nominee company — is not approximated for dramatic effect. It is accurate. The Etherington scenes, in which a stockbroker explains the leverage used against fund managers to secure IPO allocations, the concert party workarounds, the nominee companies used to accumulate Albion stock — this is detailed, surgically precise, and Churchill arrived at it in weeks. Neil Collins of the Daily Telegraph and Financial Times, a financial journalist who knew the world from inside, recognised the depth of her understanding. That authentication is what made the traders come. It is also what made the play possible as political economy rather than merely political theatre. Wolf of Wall Street, by comparison, is one-dimensional.

The structure is two acts, no formal scene breaks, though scenes have informal designations in the published text. They dissolve into each other rather than cutting. The running time is somewhere between two and two and a half hours depending on the pace of the production, which pace is itself a formal argument: the play should feel too fast, slightly out of control, a little bewildering in its accumulation of incident and voice. The confusion is not a failure of comprehension. It is the audience experiencing what it is like to be a citizen in an economy operated by people who are moving too fast for scrutiny and the friction of recall.

The formal choice that defines the play is the rhyming couplets — what the theatre scholar Janelle Reinelt precisely calls ‘the doggerel verse that Churchill adopts and wilfully abandons, or the speed it encourages, but also the scenes’ cacophony.’ Nearly the entire text is written in verse — not smooth pentameter but jangly, propulsive, variable-stress couplets that sometimes rhyme with technical accomplishment and sometimes force a rhyme with the deliberate gracelessness of a market that will take what it can get. The verse does several things simultaneously that prose cannot. It creates a distance — the Brechtian argument — that prevents straightforward identification with characters. It replicates the rhythm of the trading floor and negotiation of the boardroom, the call-and-response of dealer and counterparty, the staccato of the phone. It signals that this is a performance, a constructed thing, not a window onto reality. And it is funny, in the way that technically accomplished versification about appalling behaviour is always funny — the gap between the elegance of the form and the ugliness of the content producing a species of uncomfortable laughter.

But the Brechtian argument requires a qualification. By 1987 the alienation effect had itself been absorbed. Advertising had learned its tricks. Pop music had learned its tricks. The techniques Brecht developed to prevent audiences from consuming theatre as entertainment had been so thoroughly metabolised by consumer culture that they had become entertainment. The traders who came to the Wyndham’s were not prevented from identification by the couplets. They were delighted by them. The form that was supposed to maintain critical distance had become, in the wrong context, the form of celebration. This is not a failure of Churchill’s art. It is a demonstration of her argument: the system absorbs everything, including its own critique.

Is this her most Brechtian play? Probably yes — form and content are more thoroughly fused here than anywhere else in her work, including Top Girls. But the Brechtian inheritance is also the play’s structural irony: the more successfully the form enacts the argument, the more easily the wrong audience can consume the enactment as pleasure. Churchill knew this was possible. She did it anyway.

V. The Story, or: Everyone Is a C*nt in Some Form or Another

Churchill makes a structural decision that is both formally radical and thematically essential: there are no heroes. The play offers nobody to identify with, no conscience figure, no character who stands apart from the system and sees it clearly. Everyone is compromised. This is not misanthropy. It is political economy. In a system where the rules of the game corrupt all players equally, the introduction of a character who is exempt from corruption would be a lie.

The play opens, before its own narrative begins, with the edited Shadwell scene. Two jobbers, Mr and Mrs Hackwell, discuss investments in new patents. Whether any of the patents actually work is, Hackwell explains, entirely beside the point. The point is to generate enthusiasm for the stock — to ‘lower and heighten’ — to create volatility, because volatility is what market participants love. It makes money regardless of the direction of the price. It doesn’t help the real economy. It is built into the model. The value is in the belief, not the asset. This is Churchill saying: here is the DNA of what you are about to watch. Here it is in 1692. Here it will be in 1987. Here it will be whenever you are reading this.

The main action opens on three trading rooms simultaneously — Greville Todd (old-school broker, pitching to a client with the exact accuracy of equity sales then and now), his daughter Scilla (one of very few women on the LIFFE floor, working two phones at once), and his son Jake (dealing with his own team on yet another floor). The gilts and paper conversations that follow are staccato, transactional, minimal — cutting into the personal only when the personal is itself informational. It is utterly accurate about what a busy dealing floor sounds like and, as a result, almost entirely opaque to anyone who hasn’t been in one. Compare the same scenes in Industry, where drama is generated by interpersonal conflict and psychological revelation — gripping and insightful, but as a representation of an actual busy floor, inaccurate. Too personal. Churchill gives you the real thing. The real thing is not, in conventional dramatic terms, useful.

From here: champagne bar. Jake and Scilla discuss their plans. Jake has no intention of working after thirty. He might have to fight dirty. Enter Zac Zackerman, the American banker, the narrator-within-the-play, the figure who addresses the audience directly and explains the system while being embedded in it. Zac is Churchill’s most technically accomplished structural device: a character who functions simultaneously as participant and chorus, whose direct addresses give the audience the context they need to follow the action while demonstrating that the context itself is part of the system. He explains Big Bang, the replacement of the old British merchant bankers by the new American-trained traders, the triumph of the dealing room over the boardroom. He does it in verse. He means it entirely. And in one of the play’s most compressed and filthy lines, he summarises the imperial-to-postimperial financial transition: ‘England’s been fucking the world with interest but now it’s a different scene, I don’t mind bending over and greasing my ass but I sure ain’t using my own Vaseline.’ The British Empire exported its financial logic to the world for centuries. What Big Bang did was allow that logic to return home in American clothing and undo what remained of the British financial establishment’s pretensions to gentility. Churchill states this, through Zac, in two lines. No academic has done it more efficiently.

The plot’s spine borrows the genre mechanics of a thriller (her brother Jake in a flashback scene saying “if anything happens to me”) and then systematically betrays them. Corporate raider Corman is attempting a hostile takeover of a company called Albion — named, with Churchill’s characteristic economy of symbolism, for England. To accomplish this he needs stock bought up quietly (his broker Etherington), information from inside (Jake, feeding insider tips to Marylou Baines, American arbitrageur of supreme ruthlessness, in exchange for money). The DTI is already investigating Jake. Scilla, told by Jake the day before his death that something might happen to him, discovers his body and decides he was murdered. She investigates using his diary. In the process she meets everyone connected to the Corman deal: Jacinta Condor, the Peruvian businesswoman who has sold her copper mines and invested in coca instead; Nigel Ajibala, the African cocoa trader who has apparently internalised the colonial lesson; Biddulph, the white knight defending Albion’s chairman Duckett; a Cabinet minister who tells Corman to drop his bid until after the election; Marylou in New York; Frosby the retired jobber who, it eventually emerges, was the person who tipped off the DTI about Jake in the first place.

The investigation nominally drives Act Two. In practice it dissolves. Scilla stops looking for Jake’s murderer and starts looking for Jake’s money. ‘If it was just insider dealing,’ she tells her father, ‘it’s not a proper crime like stealing.’ Greville’s response is actually the play’s sharpest moment of inadvertent honesty: how do you define insider dealing in a world where price is a function of information asymmetry anyway? The moral arc of Scilla’s character — the play’s closest thing to a conscience — bends toward the system with the same inevitability as everyone else’s. Her final line on the subject: she had been wondering if Corman killed Jake, but now she hardly cares. ‘Fuck off, I want my money.‘

The resolution is the play’s darkest joke. Greville in jail. Corman made a Lord — and appointed Chair of the National Theatre. Duckett, who commissioned a mural titled Urban and Rural for his company that he knew nothing about, funds small orchestras. Scilla named by Business Week as Wall Street’s rising star. Jacinta marrying Zac. The final song: five more glorious years. The Tories have won the election. The system has rewarded its servants and punished only those who were unlucky or insufficiently connected. Nobody has learned anything. Nothing has changed.

The eleven rhyming couplets that close the play, each summarising a character’s fate in a single line, are among Churchill’s most devastating structural choices. The twenty-third line — ‘Frosby was forgotten’ — doesn’t scan. The broken metre of the one character who acted on something like principle is Churchill’s last formal joke: even the elegy won’t accommodate him properly.

VI. The Characters as Functions, or: The City as the Only Protagonist

The play has twenty named characters. In a real sense it has one: the City. Every individual is a function of the system, and the play’s formal structure — the overlapping voices, the multiple simultaneous scenes, the speed — prevents any single character from occupying the kind of psychological depth that would allow identification. This is not a weakness. It is the argument made theatrical.

Scilla Todd is the structural centre. She is the only character who moves through the whole play, who has an arc (such as it is), who begins with something like a moral position and ends having abandoned it. The book’s chapter on the play places her as class insider, gender outsider, then wanting to become insider — the sheer immorality of ditching her brother’s death to make money as the engine of that transformation. Scilla tells Greville his pomposity is insufferable. Greville tells Scilla she is a monstrosity. Family social relations, corrupted by greed for capital, have ceased to function as anything other than a financial negotiation. She is not primarily a victim. She is a convert. The system doesn’t destroy her — it makes her. By the end she is the system’s most efficient new recruit, which is worse.

The feminist reading of Scilla requires two passes. The first: she has to go alpha to succeed. In 1987, the first significant cohort of women in the City were operating in a world of unmediated misogyny — not the institutionally managed, HR-processed, unconscious-bias-trained version that came later, but the raw original. The trading floor was male, physically intimidating, sexually aggressive, and explicitly hostile to anyone who showed weakness. The ugliest exchanges between the male LIFFE traders in the play are, literally, explicit. To survive required performing the dominant culture better than the dominant culture performed itself. Scilla does this. She is harder, faster, and more ruthless than the men around her. This is presented not as achievement but as corruption. She is what Top Girls’s Marlene becomes when the process has run to completion — Marlene without the nightmare.

The second pass: the women in the play have, in various ways, all made it. Marylou Baines controls much of the action. Jacinta Condor deploys capital with absolute autonomy. Scilla rises. Their success does not constitute progress. It constitutes absorption. The system does not care about their gender. It cares about their function. Churchill’s argument — running from Top Girls five years earlier through Serious Money — is that the feminist politics of individual achievement is a trap. Getting women into the game does not change the game. It changes the women. And the play is closer to the reality of women in finance than most commentary acknowledges: the institutions perform diversity, but underneath is a misogyny that operates below the threshold of visibility — not in front of the women who have succeeded, which is precisely why it persists.

Zac Zackerman is Churchill’s most brilliant structural invention. As a character he is the American who comes to London and reconfigures it in Wall Street’s image — charming, technically fluent, genuinely excited by what he is doing, capable of occasional moral discomfort which he immediately overcomes. He praises London: ‘I go to the theatre, I don’t get mugged. I have classy friends.’ As a thesis he embodies the historical argument about the reversal of imperial financial flows. He ends up in bed with Jacinta, which is its own comment on how the new global financial class operates: transactions all the way down.

Frosby is the play’s Bosola figure — the malcontent, the revenger, the man who acts on something like principle from something like resentment and ends up as the system’s instrument despite himself. His speech about the old City is the play’s only elegy, and Churchill gives it in verse before breaking to prose for the moment of decision: ‘Since Big Bang the floor is bare / They deal in offices on screens / But if the chap’s not really there / You can’t be certain what he means.’ Then prose: he will report to the DTI. Frosby wants the past back. The past was also corrupt, but its corruption was legible, personal, conducted between people who knew each other. He is not wrong to prefer it. He is simply irrelevant.

Jacinta Condor and Nigel Ajibala are the play’s most politically acute characters and the ones most consistently underwritten in critical commentary. Jacinta is Peruvian, has sold her copper mines, invested in coca, and keeps her money in London because it is safe there. Her Act Two monologue is the play’s most explicit statement of the neocolonial financial circuit: the debt that will never be paid, the IMF conditionality, the flow of capital from the global south to London and New York. This is not a simplified account of the Latin American debt crisis. It is an accurate one, delivered in verse, given to a character who is herself a beneficiary of the system she describes. Jacinta is not the victim of neocolonialism. She is its local operator. And her question to Jake — after she has played every side simultaneously and he protests the deal isn’t enough — ‘What is enough?’ — is the play’s deepest rhetorical question, and Churchill leaves it hanging.

Nigel Ajibala requires more careful reading than the scholarship has given him. The standard account presents him as the postcolonial figure who has straightforwardly internalised the colonial lesson: ‘One thing one learned from one’s colonial masters, one makes money from other people’s disasters.’ This is real and the line is devastating. But there is a detail in Act Two that the scholars and critics appear to have missed. When Nigel and Jacinta are alone, she says to him: “That went very well. They can’t possibly tell. You live in a one room in a rundown hotel. I’ll buy you a silk shirt in Jermyn Street”. The implication is that Nigel’s persona — the self-made African financier who has absorbed the colonial lesson — may itself be a performance, a role played for Jacinta’s strategic purposes. He may be her paid agent, running a deeper game than anyone else in the play suspects. If so, Churchill is doing something considerably more sophisticated than the scholarship acknowledges: she is showing us the postcolonial figure as potentially a performance within a performance, raising the question of whether the ‘colonial lesson’ speech is sincere political economy or a very good line deployed by someone who knows exactly what his audience wants to hear.

Duckett, the chairman of Albion, is not the moral counterweight the plot structure seems to offer. He is not simply the victim of corporate raiding. He boasts: ‘No-one can say I’m not hard-hitting management,’ after describing sackings and redundancies — not just to improve margins, but as a performance of alpha-masculine will. You sack people as a sign of your authority, not merely your efficiency. Duckett and Corman are not opposites. They are the same psychology operating on different sides of the same transaction. Merchant capitalism and financial capitalism are different methods of extraction, not different moralities.

VII. The Genealogy: From Jonson to Churchill via the South Sea Bubble

The City Comedy proper was established, as the scholar Klaus Peter Müller notes, by about 1605, with Jonson’s Volpone, John Marston’s The Dutch Courtesan, and Thomas Middleton‘s Michaelmas Term as its founding texts. It is a form born of a specific historical moment: the early development of a commercial economy in London, the emergence of a new class of merchants and financiers, the collision between inherited aristocratic values and the new logic of the market. It asks what happens to human beings when money becomes the measure of all things. The Roman comedy tradition — Plautus, Terence — is the deeper ancestor, and the ‘types’ of City comedy (the gulled merchant, the clever servant, the woman who outmanoeuvres the men) are themselves inherited types that Churchill refills with contemporary content. The tradition is that long.

Jonson’s answer is to make greed theatrically magnificent. Volpone is not simply corrupt — he is artistically corrupt, a performer of genius whose scam is itself a kind of art form, whose joy is in the playing rather than the winning. The Alchemist runs the same logic: the con is an improvised theatre, the three charlatans endlessly inventive, the queue of gulls a parade of human weakness that is simultaneously contemptible and irresistible. There is energy in Jonson’s greed, a carnival vitality that keeps his plays alive four centuries later not because we admire the villains but because we recognise the theatre of what they are doing.

Churchill’s traders are not Jonsonian gallants. Müller is correct about this, but the observation requires extending. The Jonsonian gallant wants wit allied with money — a style of living, a performance of superiority, the con as aesthetic experience. The post-Big Bang trader wants to win. The game is not the vehicle for the performance of selfhood. The game is the point, and the money is the scorecard that tells you whether you won. This is a historical shift in the psychology of avarice, and it is what makes 1987 City comedy formally different from 1605 City comedy even when it shares the genealogy and the subtitle.

The difference also shows in the formal texture. Jonson’s prose is dense, allusive, linguistically spectacular — language as conspicuous consumption, rhetoric performing the excess it describes. Churchill’s couplets are fast, functional, occasionally deliberately ugly. They replicate the rhythm of the floor rather than the language of wit. Where Jonson’s characters talk their way into the scam, Churchill’s characters talk their way through the deal. The pleasure is kinetic rather than rhetorical. The speed is the form.

Churchill also inherits from Jonson the formal problem of when to stop. Jonson notoriously didn’t know — Bartholomew Fair, The Alchemist, Volpone all continue past the point where a neater playwright would have ended them. The excess of incident is itself the argument: the market never stops, there is always another transaction, the system has no off switch. Serious Money has this quality too. Twenty characters, multiple scenes across two acts that accumulate rather than build toward climax. Critics who find it too long are technically right and critically wrong. The length is the argument. More is more in the City. There can never be too much information, too much data, too much narrative.

VIII. The Couplets: Form as Argument

Let us be specific about what the verse does, because the standard account — it creates Brechtian distance, it replicates market rhythm, it places the play in the City Comedy tradition — is true but incomplete.

The couplets commodify language. This is the deepest formal argument. In a market, everything is priced: labour, land, futures, options, the right to buy something that doesn’t exist yet at a price agreed today. Churchill’s verse structure does to dialogue what the market does to human activity — it packages it, gives it a unit of exchange (the couplet), makes it tradeable. Every line requires a rhyming completion, which means every statement is in a relationship of dependency with the next. The form enacts the transactional logic it describes.

The verse also does something to tone that prose cannot manage: it holds comedy and horror simultaneously. Jacinta’s lines about closing her mines — ‘I lose every quarter / The cash goes like water / Is better to close the mine’ — have the meter and bounce of a nursery rhyme. The content is the destruction of livelihoods. The gap between the form’s lightness and the content’s weight produces a species of laughter that is also a species of revulsion — and crucially, you cannot have the revulsion without the laughter, because if the content were delivered in prose it would read as political speech and invite a different, more comfortable kind of response. The verse makes the audience complicit in finding atrocity funny. This is Churchill’s most precise formal achievement.

The play’s single most extraordinary line is Scilla’s description of the LIFFE floor: ‘On the floor of LIFFE the commodity is money / You can buy and sell money, you can buy and sell absence of money.’ Consider what this means. The derivatives revolution — not new in 1987, LIFFE had been operating since 1982, but accelerating fast — had created instruments that were not claims on assets but claims on future prices: futures, options, swaps. You are trading not a thing but the right to buy or sell a thing at a future price, which is the financialisation of time itself. And then: ‘absence of money.’ A short position. A bet that something will lose value. The financial system has made the non-existence of a thing into a tradeable commodity. Churchill renders this in two rhyming lines. Was the floor of LIFFE — Life — a joke? Almost certainly deliberate. The floor of life is where you trade absence. Harvey’s compression of time and space is right there, in verse, in 1987.

The verse breaks down at specific moments, and the breakdowns are the play’s most important formal events. Aggression and genuine threat tend to break the verse: Corman threatening Marylou abandons the couplets, the real self behind the performance surfacing when the game becomes visceral. Frosby’s confession that he reported Jake to the DTI is delivered in prose after a scene of verse — the formal constraint drops at the moment of genuine moral action, as if the system’s rhythm cannot contain what he is saying. The verse resumes almost immediately. The system reasserts its form over the individual who momentarily escaped it.

The songs are a third formal register and deserve their own consideration. Ian Dury’s music — punk-inflected, class-conscious, cheerfully obscene — connects the play to a parallel vernacular tradition running from the broadside ballad through the music hall through punk: the popular song as social commentary, the form that tells uncomfortable class truths in a register the establishment can’t quite object to because it’s entertainment. Dury is, in this sense, more 1605 than 1985 — the tradition is that old. The Act One closer celebrates the LIFFE floor with pure energy and zero critical distance. The Act Two closer — five more glorious years — is the same energy in a different key, which makes it more disturbing. The traders’ celebration of Thatcher’s victory is formally identical to the traders’ celebration of their own competence. Churchill is showing you that these are the same thing.

IX. The Audience Problem, or: Who Is Laughing and at What

The scholar Klaus Peter Müller, writing in Modern Drama in 1990, identified what he called the play’s interesting social and theatrical phenomenon: financiers, brokers, traders and arbitrageurs came in droves to gleefully watch their life presented on the stages of, first, the Royal Court Theatre in Chelsea and then, in greater numbers, the Wyndham Theatre in the West End. He notes that newspapers puzzled over this, and offers the framing of two alternatives: either people were blindly dancing on a volcano, or we were confronted with a postmodernist variety of conscious indulgence in one’s own sins.

Both framings are wrong, or at least insufficient. Blindly dancing on a volcano implies ignorance that wasn’t there. Conscious indulgence implies ironic self-awareness that overstates the sophistication of the response. What actually happened was more interesting and more revealing.

The play transferred from the Royal Court to the Wyndham’s in July 1987 — between the two runs, Thatcher won her third election, providing the play with a real-world Act Two closing song. The Royal Court is a subsidised theatre in Chelsea with a specific constituency: the left-cultural intelligentsia, theatregoers who consider themselves politically engaged, people who go to the theatre partly as an act of cultural citizenship. They came to see themselves confirmed in their analysis of what Thatcherism was doing to Britain. They got that, and it was extremely well written, and they were happy.

The Wyndham’s is a commercial West End theatre. It does not have a political constituency — it has a market. By the time Serious Money transferred there, it had a reputation: the hot ticket, the play everyone was talking about, the thing you had to see. City workers came because it was about them, because their colleagues had been, because not having seen it was becoming a social liability in the clubs and bars around EC2. They came, and what they found was an accurate portrait of their world, delivered in a formal register they could recognise as entertainment, at speed, with funny lines and songs and characters who were clearly caricatures of people they actually knew.

They laughed. They cheered. The reports are consistent on this. Thomas Sutcliffe in the Independent put it with memorable precision: ‘It’s now a bit like going to see The Resistible Rise of Arturo Ui with a coach party of SS men.’

What were they laughing at? Not at themselves in any straightforwardly self-critical sense. They were laughing at an accurate representation of a world they inhabited and felt proud of inhabiting. The laughter is the laughter of recognition — this is us, we are real, our world is real enough to be the subject of a major play. It is also, and this is the key thing, the laughter of a club — a demonstration of belonging, of being among people who know the references, who understand the jargon, who get the joke because they are the joke. In 1988 some LIFFE traders famously stood on a balcony outside the Stock Exchange and waved fifty-pound notes at a crowd of protesters below. That image — raw, unguarded, entirely without shame — is the correct frame for understanding the Wyndham’s laughter. It is not the laughter of people who think they might be wrong. It is the laughter of people who know they are winning and find the idea of criticism delightful because they are immune to it.

The financial success of the production compounded the irony. Serious Money became serious money for the Royal Court — a sell-out from the start, a commercial triumph that Churchill’s old collaborator Pam Brighton of Monstrous Regiment called bourgeois. Stafford-Clark acknowledged it openly. Wyndham’s investors made money. The radical play that anatomised the market was processed by the market and returned a profit. Capital invaded the production as it had invaded the audience. Churchill was reportedly in some denial about the extent of this — she felt the press had exaggerated the City-audience phenomenon. She may have been right about the scale. She was not right that it didn’t matter.

This is the complicity problem that Churchill could not solve, and that no satirist working inside the entertainment economy can solve. Satire requires the target to be embarrassed. Embarrassment requires a social consequence for the behaviour being satirised. In 1987, for City workers, there was none. The play’s critique had no teeth because the behaviour it criticised was being simultaneously rewarded by every other institution in the country. Churchill could not have written the play differently and made it land on the Wyndham’s audience as critique rather than celebration. The problem is structural: once the play entered the entertainment market, the entertainment market processed it according to its own logic. Which is, of course, exactly what the play is about.

The Broadway failure, after an off-Broadway success, is illuminating by contrast. The same production — directed by Stafford-Clark, with a serious cast including Alec Baldwin and Kate Nelligan, produced by Joseph Papp for the New York Shakespeare Festival in association with the Shubert Organization — opened at the Royale Theatre on 9 February 1988 and closed after fifteen performances. The American financial industry embraced it in their own way: the Securities Industry Association sponsored one night, major bankers and Federal Reserve representatives attended, the opening night party was held on the trading floor of the COMEX. The industry came. General Broadway audiences did not. American theatre culture in 1988, and maybe still now. was not equipped for a play with no resolution, no moral redemption, no hero, and an ending that celebrated the bad guys’ electoral victory. There is a further irony: the play is specifically about the Americanisation of the City. Zac is the American export. American audiences watched a critique of their own export and stayed away. The Zacs of the world were in the Wyndham’s, laughing. Their country of origin was at the Royale, unmoved.

X. The Genre After Churchill: Or, Why the Founding Text Remains Unsurpassed

The finance play is a thin genre. This requires explaining, because the dramatic material is manifestly rich: the stakes are vast, the behaviour is extreme, the jargon provides a kind of poetry of the inhuman, and the events of the last four decades have provided more dramatic material than any playwright could process in a career. And yet the tradition from Serious Money to the present is sparse, and nothing in it has matched what Churchill did in 1987.

The genre fails, when it fails, in one of three ways. The morality problem: the writer wants to avoid polemic and produces characters with rounded motivations, and rounded motivations in a financial context produce sympathy where critique should be. Jerry Sterner’s Other People’s Money (1989) is the clearest example. Larry the Liquidator has good lines and genuine energy, but the play’s debate structure — Larry versus Jorgy, market logic versus community values — implies the question is genuinely open. It isn’t. The play makes some good points and gets a fair few wrong and gets bogged down in cliché. Churchill’s answer to the morality problem was to refuse it: distribute the corruption so evenly that identification becomes impossible, and let the system rather than any individual be the object of critique. Most finance drama since has been too timid to do this.

The comprehension problem: the jargon barrier is real but secondary. The deeper issue is that financial instruments are genuinely abstract and resistant to theatrical representation. Lucy Prebble’s Enron (2009) solved this with theatrical invention — the Raptors, the dancers, the spectacular staging — and produced the most formally interesting post-Churchill finance play. But Enron was a smash in London and struggled in New York. The comprehension problem is not really about understanding derivatives. It is about theatrical language and systematic narrative.

Enron is specifically about American corporate culture and American institutional failure — but Prebble is British, the production aesthetic is British, and the formal devices read as clever British meta-theatre. There is a mild cultural condescension problem that the London production didn’t have. More importantly: American theatre culture has a structural difficulty with plays that offer no redemption and no individual agency. The GFC produced enormous anger in America but it also produced enormous denial — the narrative that it was caused by individual bad actors (Madoff, specific bankers) rather than systemic failure was far more culturally available in America than in Britain. A play that insists the system is the problem rather than the individuals is harder to receive in a culture that is ideologically committed to individual agency as the explanatory frame. Finally again Broadway economics: a technically complex, formally experimental British play about a corporate scandal requires an audience willing to do work. That audience exists in London’s subsidised theatre ecosystem. Broadway’s commercial economics demand broader appeal.

The temporal problem: finance operates faster than theatre. By the time a play about a specific financial scandal reaches the stage, the scandal has moved on. This is the reason most finance plays date badly: they are accurate about the specific event and wrong about the system, when Churchill was wrong about nothing systemic. Serious Money does not date because it was never primarily about Big Bang. It was about the system that produced Big Bang, has continued to produce it, and will go on producing it. The critics of 1987 saw the surface. The surface has dated slightly. The structure hasn’t, because the structure is about how the system thinks, or rather how it prevents thinking, which turns out to be one of the permanent features of the thing.

The Lehman Trilogy (Stefano Massini, adapted Ben Power, directed Sam Mendes, NT 2018) is a different beast and should not be placed in direct competition with Serious Money. It is elegiac where Churchill is diagnostic, tragic where she refuses tragedy. Mendes’s production was extraordinary: three actors, a piano, a revolving glass box, one hundred and sixty years of American capitalism compressed into three hours of theatrical sublimity. It mourns. Churchill refuses to mourn. The refusal is the argument.

Sarah Burgess’s Dry Powder (2016, Hampstead 2018) is the most technically accurate contemporary finance play after Serious Money — accurate about private equity culture, precise about the language, genuinely funny in places. It gives you the texture of the world without quite making the formal argument that the texture constitutes an indictment. Burgess knows her subject; she doesn’t quite know why the subject matters. Glengarry Glen Ross (David Mamet, 1982) belongs in the genealogy obliquely — it is about sales rather than finance, and it is about the American salesman as a tragic figure, and tragedy requires the possibility of dignity. Churchill’s traders don’t have dignity to lose. They have price.

The founding text of the modern finance play genre was written in 1987 and remains unsurpassed. The genius Caryl Churchill nailed it and nobody has matched it since. This is not a dismissal of Prebble or Massini or Burgess. It is a claim about the depth of the analytical framework underlying the formal achievement. You cannot write a play this accurate about the system unless you understand the system. You cannot make that accuracy theatrically powerful unless the form enacts the understanding. Churchill did both simultaneously, in seven weeks.

XI. What the Critics Saw and What They Missed

Serious Money received mixed reviews on its initial run — sell-out from the start, but the critical reception was not unanimous. The Sunday Times called it brutally brilliant, savagely funny and appallingly realistic. The Daily Telegraph gave it the authentication that mattered most: the first play about the City to capture the authentic atmosphere of the place. Neil Collins, writing with the authority of a financial journalist who knew the world from inside, recognised what Churchill had achieved. The Olivier Award for Best New Play confirmed the establishment’s verdict.

What the critics mostly saw was topical satire of extraordinary quality: a brilliant account of a specific moment that would obviously date as the moment receded. This was the consensus, and it was wrong in the way that consensuses about contemporary art are reliably wrong: accurate about the surface, blind to the structure.

What the critics missed: the global dimension. Jacinta and Nigel were read as colourful secondary characters providing comic relief and exotic texture. They are actually the play’s most precise political economy. The neocolonial circuit — Peruvian copper, African cocoa, Latin American debt, IMF conditionality, the flow of capital from the global south to London and New York — is not background. It is the explanation. The City doesn’t just exploit the British. It exploits everyone, everywhere, continuously, and the people it has historically exploited have learned its methods and joined the queue. This analysis was not available to the British theatre critics of 1987, who were watching a play about the City and thinking about Britain.

What the critics also missed: the feminist argument’s full depth. The play was praised for having strong female characters and for depicting the sexism of the financial world. This is true but thin. Churchill is not making the modest argument that the City is sexist. She is making the structural argument that the system absorbs women and that absorption is more insidious than exclusion, because it forecloses the possibility of a feminist politics of solidarity. Scilla doesn’t need solidarity. She has the game.

What the critics could not have seen in 1987 is the play’s “prescience” — not about specific events but about structural tendencies. The financialisation of everything: the process by which financial logic colonises domains previously organised by different principles — healthcare, education, housing, culture, personal relationships. Churchill doesn’t use the word. She shows the process. Every revival since 2008 has been greeted with the observation that the play is more relevant now than when it was written. This is true but needs refining: the play was not “prescient” about what would happen. It was accurate about what was already happening and had always been happening. The critics of 1987 thought they were watching a document of a specific moment. They were watching a diagnosis of a permanent condition. Churchill invariably does this.

XII. The Period Piece Problem and Why It Is Not One

A recurring motif in reviews of Serious Money revivals is the simultaneous claim that the play is more relevant than ever and that it is a period piece. A review of the Birmingham REP production over a decade later put it plainly: the lines about greed and recession probably have more relevance now than when they were written, but you are reminded towards the end that it is a period piece when a character pleads about Tebbit and the Tories celebrate five more glorious years.

This is a failure of critical nerve disguised as even-handedness. The Tebbit reference and the Thatcher celebration are not period markers that date the play. They are structurally essential to its argument. The argument is precisely that electoral politics provides legitimacy and cover for the financial system to continue regardless of any other social consideration. Gleason, the Cabinet minister who meets Corman at the NT during the interval of King Lear — the greatest play about the destruction of a kingdom by greed and ambition running onstage without him — and tells Corman to drop his Albion bid until after the election, is not a dated figure. He is a permanent one. The system has always required political protection. In 1987 it was provided by Thatcher. In subsequent decades it was provided by her successors of all parties. The specific names change. The structural relationship does not.

The final song is dated only in its specific reference to the 1987 election. As a structural statement it is timeless: the system celebrates its own continuation, and the celebration sounds identical to entertainment, and the audience cannot tell the difference because there is none. The system always has five more glorious years. That is what systems do.

The period piece argument is also a symptom of a problem that Churchill herself diagnosed: the general eluding audiences who are stuck in the particular. Bright, engaged people taken to see Top Girls read Marlene as a specific type of woman they recognised from the 1980s. They did not read her as a structural argument about capitalism and feminist politics. They were stuck in the particular. The same thing happens with Serious Money: audiences who are financially literate see 1987, see the specific instruments and institutions of that moment, and register the period detail as datedness. Audiences who are politically literate see the system those instruments and institutions were expressions of, and recognise it as permanent. Churchill requires both kinds of literacy simultaneously. That is the narrow Venn diagram problem, and it is real, and it is worth being honest about. The socialist luvvies who adore her supply both kinds of literacy. The rest of the audience — the bewildered civilians, the exhausted City workers who came because their colleagues had — supply one kind at most. The canonical status of Serious Money reflects the literary taste of the Venn diagram’s narrow centre. That is not a criticism. It is a fact about how canons form.

XIII. Afterlives: The Allure of Finance and the Culture It Made

The traders who came to the Wyndham’s in 1987 have had descendants in every medium since. The cultural afterlife of the world Churchill anatomised is enormous, and the recurring pattern across it — the intended critique consumed as celebration — is her argument demonstrating itself in real time.

The Wolf of Wall Street (Martin Scorsese, 2013) produced a phenomenon structurally identical to the Wyndham’s one: an exposé received as a how-to guide by one audience and a nostalgia object by another. Wall Street screening parties with 1980s fancy dress. Leonardo DiCaprio as aspiration. The critical reading — this is a portrait of moral vacuity — was structurally unavailable to anyone who wanted to be the person on screen. Oliver Stone‘s Wall Street opened during the New York run of Serious Money in 1987, the two works occupying the same cultural moment from different media. Stone intended critique. He got Gordon Gekko as a cultural hero.

Jesse Armstrong‘s Succession (HBO, 2018-2023) is the most sophisticated recent engagement with the same material. The Roy family are not City traders — they are media-finance dynasty, a different register — but the psychological and structural analysis is Churchillian in its refusal of heroes, its systemic rather than individual account of corruption, its formal use of black comedy to hold horror and entertainment simultaneously. The difference: Succession is pessimistic tragedy about a specific family. Serious Money is something harder — it is not tragic because nobody is diminished. The system works exactly as designed, and its working is not a tragedy. It is a normal Tuesday.

Mickey Down and Konrad Kay‘s Industry (BBC/HBO, 2020-) is closer to the Serious Money world in setting: young graduates at an investment bank, the culture of the floor, the performance of competence under pressure, the psychological cost of the game. It is genuinely good television and it gets the culture right in ways that most finance drama doesn’t. But what Industry cannot do — because it is a character drama, because it must give its characters psychological depth to sustain multiple series — is make Churchill’s argument. Individual psychology is the wrong unit of analysis for what Churchill is describing. Industry shows you what it costs to be a person in the system. Serious Money shows you what the system costs everyone else.

The most interesting afterlife is the one nobody has written. The play about the 2008 crisis that is equal to Serious Money — that captures the crash with Churchill’s combination of formal invention, structural analysis, and refusal of comfort — doesn’t exist. David Hare tried with The Power of Yes (2009), an earnest documentary-drama that explains the crisis to a lay audience. It is useful and well-written and it is approximately the opposite of Serious Money: patient where Churchill is frantic, explanatory where Churchill is satirical, responsible where Churchill is furious. Both are necessary. One of them is art.

There is also the question of the capital that now funds the institutions that produce work like Churchill’s. The Royal Court, home of radical writing, occupies one of London’s most expensive postcodes. Its corporate sponsors and major donors increasingly come from the financial markets world — hedge fund trusts and their philanthropic arms. The irony of radical theatre sustained by the money it is supposed to be critiquing is not lost on everyone. It was already there in embryo in 1987, on the day Stafford-Clark sat down with Thatcher to discuss arts subsidies. The market invaded the institution that was critiquing the market. The play became serious money for the Royal Court. Capital invaded this process as it had invaded the audience. Exposing capital, embraced by capital, exhausted by capital: the trajectory of the play’s original run is also the trajectory of the theatrical institutions that produced and benefited from it.

XIV. The Mouse-Trap

The first jobber in the Shadwell scene describes the financial system: It is a Mouse-Trap, designed to attract all mice, and even rats, regardless of their consent.

This is Churchill’s frame for everything that follows. The trap is designed. It attracts regardless of consent. The mice who enter it are not stupid — they know it is a trap in some abstract sense. They enter anyway, because the trap has been constructed to make entry feel like freedom, like intelligence, like the exercise of skill and nerve that separates the quick from the slow. The mouse that is caught believes, right up to the moment of the snap, that it was winning. That there is a greater fool, and that it is not them.

Caryl Churchill wrote this play in 1987. She was forty-nine. She had been watching for forty-nine years. She collected newspaper cuttings until the cuttings looked too much like a research paper and she put them down and wrote a play instead, in seven weeks, in rhyming couplets, with songs by the working-class Essex boy whose vernacular social commentary belongs to a tradition as old as the broadside ballad. The play opens in 1692 and ends in 1987 and is set in a permanent present that recurs every time the market collapses and recovers and someone young and clever and hungry arrives at the trading floor believing that this time it will be different because they are smarter than everyone who came before. That there is a greater fool, and that it is not them.

The traders who cheered at the Wyndham’s were not wrong to cheer. They were in the trap and they were winning. They kept winning for a while. In October 1987, while Serious Money was running, Black Monday erased twenty-three percent of the Dow in a single day. The greater fools had disappeared. The play had a reference added for the Broadway transfer. The production kept running. The system kept running. It always keeps running. That is the point.

The trap never closes. It only snaps on some of the mice some of the time. The rest go on attracting the next generation. The play goes on being revived. The analysts go on arriving at the desk at six in the morning. The derivatives go on accumulating notional value. And somewhere, in the section of the audience that is not socialist luvvies and is not bewildered civilians and is not exhausted City workers who came because their colleagues had, there is a narrow group of people with the right combination of financial literacy and political consciousness and theatrical sophistication, and for them Serious Money is as good as anything written for the stage in the past hundred years, and they know exactly what Churchill was laughing at when she wrote it.

She wasn’t laughing at the traders. She was laughing at a country that knew the trap was there and walked in anyway, every generation, and called it progress.

—

A Note on Sources and the Reading of the Play

The primary source for this essay is the published text of Serious Money, in Churchill Plays: Two (Methuen Drama). Quotations from the text are taken directly from a reading of the play and verified against secondary sources. The scholarly foundation draws on Klaus Peter Müller’s ‘A Serious City Comedy: Fe-/Male History and Value Judgments in Caryl Churchill’s Serious Money’ (Modern Drama, September 1990); the Cambridge Companion to Caryl Churchill (Aston and Diamond, eds., 2009); Elaine Aston’s monograph Caryl Churchill (Northcote House); Linda Kintz’s ‘Performing Capital in Caryl Churchill’s Serious Money’ (Theatre Journal, October 1999); and the chapter ‘Derivative: of Capitalism or the Theatre’ in The Theatre of Caryl Churchill. The Marandi and Anushiravani article in English Language and Literature Studies (2015) provided useful textual quotation. Production history from Theatricalia and IBDB. Reviews from the Sunday Times, Independent, Daily Telegraph, Time Out London, Time Out New York, and the British Theatre Guide.

A note on the personal testimony in this essay: the writer used to work in an investment bank with direct professional knowledge of the market culture the play depicts and has attended multiple productions including the original West End run and the LAMDA production in 2019. That professional context informs the reading throughout and constitutes, alongside the scholarship, one of the essay’s two primary methodological foundations. As with other pieces in this series, the intellectual architecture is collaborative — the method is disclosed in the standard note elsewhere on this site.

Leave a comment