Essays in Dignity and Political Economy

These essays are written in dialogue between a human thinker and an AI interlocutor. The thinking is collaborative. The voice and the judgement are human. The form is the argument. There are gaps. Help us fill them.

The manifesto these essays argue toward — Listen to Me — is already published on this blog.

Essay Six A — The Arithmetic of Care

Pensions, Healthcare, Social Care and the Honest Conversation Our Politics Cannot Have

A note before we begin.

This essay has been sitting on the production schedule for longer than any other in this series. That is not accidental.

The previous essays have been difficult in the ways that political economy is usually difficult — requiring the reader to think carefully about things they would rather not examine too closely. This one is different. Care — in its broadest sense, encompassing what we spend on the elderly, the disabled, the sick, and those who look after them — sits at the precise intersection of economics, personal morality, social ethics and political ideology. Every position on it implies something about what we owe each other, what the state is for, what a life is worth, and who should bear the costs of human vulnerability.

These are not questions with clean technical answers. They are questions about values. And reasonable people with good intentions hold genuinely conflicting values when it comes to them.

We also cannot discuss care without discussing pensions and healthcare. They are not separate problems. They are three dimensions of the same structural question — what does a society owe its members across the full arc of a human life, and how does it pay for it? Separating them, as public debate usually does, is part of why the conversation stays confused.

So this essay will proceed carefully. But it will proceed. The reason these questions get put off is not that they are too hard to think about. It is that thinking about them clearly forces choices that our current political system is structurally incapable of making honestly. Politicians know this. Civil servants know this. The Treasury knows this. The think tanks have known this for thirty years. The knowledge has not produced action because action requires an honesty that the electoral cycle punishes.

That is not a reason to avoid the thinking. It is the reason the thinking matters.

We do not intend to offend. But by definition this is uncomfortable. If it were not, someone would have sorted it out by now.

One more thing. This is not a party political argument. The failures described here span governments of both major parties across four decades. This is a systemic problem not a partisan one. Though it does have ideological dimensions that we will name plainly when we get to them.

Now. The numbers. As best we can.

Part One: What the State Raises and What It Spends

Before we get to care specifically, the full fiscal picture is necessary context. Most public debate about public spending proceeds without it, which is why most public debate about public spending generates more heat than light.

The UK government in 2024/25 raised approximately £1.1 trillion in tax revenue and spent approximately £1.28 trillion — a deficit of roughly £130 billion funded by borrowing. Tax revenue as a share of GDP is around 36-37%, which is historically high for the UK but considerably lower than most comparable European economies. France raises approximately 46% of GDP in tax. Germany 39%. Denmark 46%. Sweden 42%. The UK sits in the lower half of the European distribution while expecting outcomes that require the upper half.

Where does the money go?

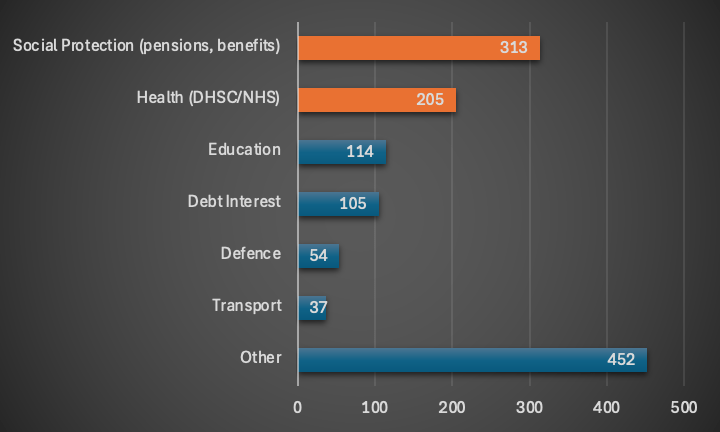

CHART 1: UK Government Spending by Category 2024/25, (£bn)

Source note: HM Treasury/OBR

The numbers that matter most for this essay are the top two. Total welfare spending in 2024/25 was approximately £313 billion — around 24% of all government expenditure. Of this, approximately £150 billion — nearly half — was spent on pensioners, including the state pension, pensioner housing benefit, pension credit and the winter fuel payment.

This figure covers state pension and related welfare payments to pensioners. It excludes the annual cost of public sector defined benefit pension payments — approximately £50-60 billion sitting within departmental budgets — and the cost of pension tax relief, which at approximately £48 billion annually is one of the largest and most regressive tax subsidies in the system, delivering 40p of relief per pound contributed to higher rate taxpayers and 20p to basic rate taxpayers. The full cost of pension provision to the public finances is considerably higher than the welfare headline suggests.

The Department of Health and Social Care’s budget in 2024/25 was £204.7 billion, the vast majority of which — £187 billion — was allocated to NHS England.

Adult social care spending by local authorities in England in 2024/25 was £34.5 billion — an increase of 7.9% in cash terms from the previous year.

Together these three — pensions, healthcare and social care — consume well over half of all government spending. They are the core of the postwar social settlement. And they are all under structural pressure from the same source.

Part Two: The Three Promises and the Demographic Problem

The postwar settlement made three promises simultaneously. The NHS — universal healthcare free at the point of use. The state pension — income in retirement regardless of individual savings. And social care — support for those who cannot support themselves.

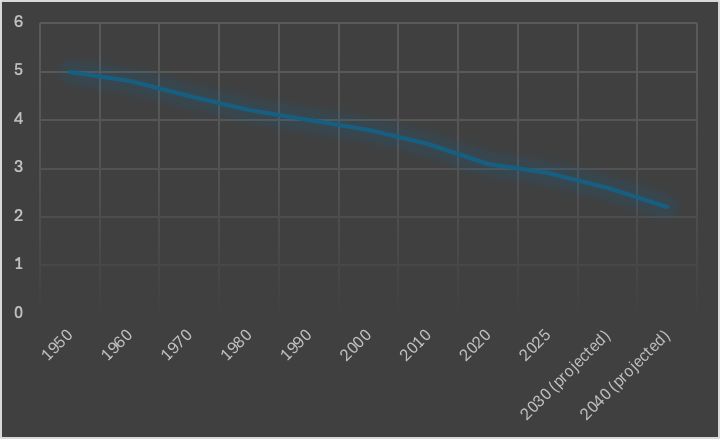

These promises were made when the demographic pyramid had the right shape. Many working-age people paying tax to support relatively few elderly dependants. The ratio in 1950 was approximately five working-age people for every person over 65. It is now approximately three to one. By 2040 it will be closer to two to one.

CHART 2: The Demographic Inversion — ratio of working-age population to over-65s, 1950-2040

Source note: ONS

The number of people aged 65 and older in England and Wales increased from 9.2 million in 2011 to more than 11 million in 2021. That increase of nearly two million happened in a decade. The next two decades will see larger increases as the baby boom generation moves fully into old age.

The promises remain. The arithmetic is changing. This is the structural problem that nobody in mainstream politics will state plainly before an election and everybody knows about afterwards.

The three promises were never fully funded in the way that a private pension or insurance scheme is funded. National Insurance — despite its name and despite the widespread belief that it functions like a contributory savings system — was always a pay-as-you-go arrangement. Today’s workers pay today’s pensioners and today’s NHS costs. There is no pot with your name on it. There never was.

This is not a scandal or a deception. It is how all pay-as-you-go social insurance works. But it does mean that the system’s sustainability depends entirely on the ratio of contributors to recipients — and that ratio is moving in the wrong direction.

Part Three: What Care Actually Costs — and Who Actually Pays

Within this broader picture, social care has a specific and largely hidden problem. It is the least visible of the three promises and the most inadequately funded.

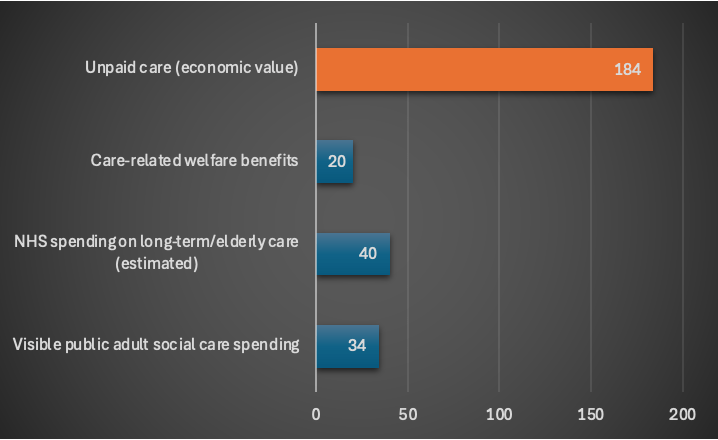

Total adult social care expenditure in England rose to £34.5 billion in 2024/25. But this is only part of the true cost. In real terms, spending is 29% higher than in 2015/16. Despite recent increases it has not kept pace with rising demand.

The reason it has not kept pace is that the largest component of care provision does not appear in the government accounts at all.

The economic value of unpaid care provided by family members and friends across the UK is now estimated at £184 billion per year. To put that in perspective it is roughly equivalent to the entire NHS budget. It is provided by approximately 5 million people who receive no payment and minimal support for doing so.

CHART3: The True Cost of Care — visible public spending versus unpaid care value, (£bn pa)

Source note: King’s Fund, Carers UK/Centre for Care, HM Treasury

Unpaid carers contribute the equivalent of four million paid care workers to the social care system. Without them the system would collapse overnight.

Who are these people? 10.3% of women provide unpaid care, compared with 7.6% of men, and the gap widens considerably among those providing intensive care of fifty or more hours weekly. The older woman caring for an older partner or parent is the invisible foundation on which the entire system rests. 1.2 million unpaid carers live in poverty. 400,000 live in deep poverty. 69% of carers who are employees say they have not focused on their career as much as they would like.

The people doing this work are not receiving dignity. They are subsidising the system that is supposed to provide it.

And the paid care workforce fares barely better. Median care worker pay as at December 2024 was £12.00 per hour — sitting just above the 10th percentile of the whole economy. The people doing the most important work in the building are paid at the bottom of the distribution. This is not a market signal. It is a political choice about whose work counts.

Part Four: The Self-Funder Trap

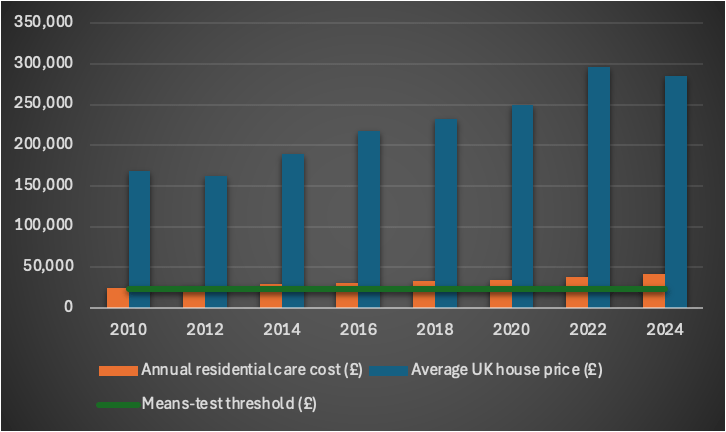

For those who do require formal care — in a care home or through intensive home care — the system operates through a means test that has not been meaningfully updated in fourteen years.

The capital threshold above which you must fully fund your own care has remained at £23,250 since 2010 — frozen for fourteen consecutive years. Average household wealth in Great Britain grew by 50% in cash terms in the decade to 2020. The threshold was set for a world in which average house prices were considerably lower and asset accumulation was less widespread. It now catches people who are not wealthy by any reasonable definition — people who bought modest houses, saved carefully and did everything they were told they should do. Their prudence is the system’s funding mechanism.

Current average care home costs in 2025/26: residential care approximately £800 per week, nursing care £1,100 per week, dementia care £950 per week — significantly higher in London and the South East.

At £800 per week, residential care costs approximately £41,600 per year. The average stay in a care home before death is approximately two and a half years. That is over £100,000 for an average stay — and considerably more for nursing or dementia care, or for longer stays.

The government had planned to introduce a lifetime cap on care costs in England of £86,000. This plan was scrapped in July 2024. Care home fees for self-funders rose by 10% between December 2024 and December 2025.

CHART 4: The Self-Funder Trap — frozen threshold against rising care costs 2010-2024, £

Source note: DHSC, ONS House Price Index, Laing Buisson/Which? Care data. Note: Threshold frozen at £23,250 for 14 consecutive years.

Part Five: What the Rest of Europe Spends

The standard response to any of this from the political right is that we cannot afford more. The standard response from the political left is that we must spend more without specifying where the money comes from. Both are inadequate. And both contain a contradiction that deserves naming before we get to the data.

The right’s position is this. Taxation is already too high. The state is too large. Individual responsibility and private provision are preferable to collective solutions. The family home is a sacred inheritance that the state should not touch. Care costs should not consume the assets that people have worked hard to accumulate and intend to pass on to their children.

This is a coherent ideological position. It has one problem. The people who hold it also, in overwhelming numbers, support the NHS, the state pension and some form of collective care provision. They use these services. They depend on them. They would be furious if they were removed. The ideology says the state should be smaller. The revealed preference says the state should keep providing everything it currently provides. These two positions cannot be simultaneously maintained without either raising taxes or running up debt that future generations will pay. The right has spent four decades pretending otherwise. Or pretending that “efficiency” gains will bridge the gain without a shred of evidence It has not worked. The care crisis is partly the accumulated consequence of that pretence.

The left’s position is this. The state must spend more on care. Care workers must be paid properly. Unpaid carers must be supported. The system must be adequately funded. All of this is correct.

The left then tends to gesture toward taxing the wealthy as the funding mechanism. Also correct in principle. But the arithmetic of taxing only the super-rich to fund the full cost of adequate care, pensions and healthcare does not work. The numbers are not there. The top 1% of earners in the UK pay approximately 29% of all income tax. Extracting significantly more from them is both politically difficult and arithmetically insufficient for the scale of the challenge. Adequate collective provision requires adequate collective contribution — which means the broad middle as well as the wealthy top, uncomfortable as that is for a politics that has learned to promise more while asking less.

The specific contradiction on inheritance is worth dwelling on. Both sides perform gymnastics around it. The right defends inheritance as the natural extension of the property rights it champions — you earned it, you should be able to pass it on. But the asset wealth that most middle England families hope to inherit was not primarily earned. It was inflated by rising house prices driven by planning restrictions, low interest rates and financialisation — none of which the inheritors created. The right is defending the transmission of unearned windfall gains while opposing the taxation that would fund the care that made those gains possible in the first place. The NHS kept the asset-holder alive long enough to accumulate the asset. The care system will be needed to support them at the end. The inheritance that the right wishes to protect is partly a product of the collective provision it wishes to starve.

The left, meanwhile, wants to tap asset wealth — but only above a threshold that conveniently excludes the aspirational middle who also vote in elections. The political calculation is the same as the right’s, just drawn at a different income level. Neither side will say plainly that adequate collective provision requires a broader fiscal base than either is currently proposing.

Now the data.

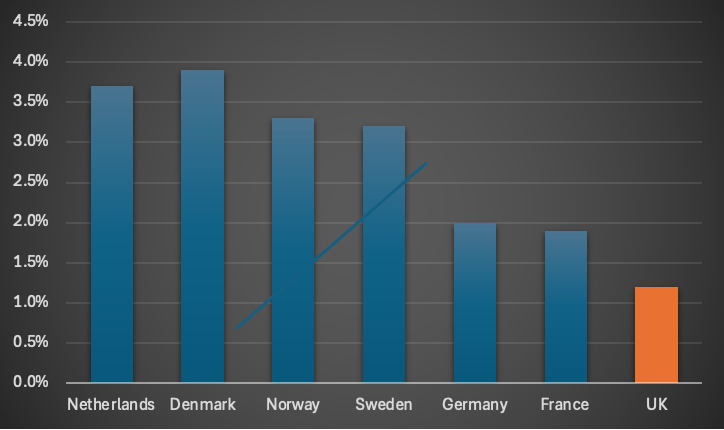

CHART 5: Long-Term Care Spending as % of GDP, Selected Countries

Source note: OECD Health Statistics 2023. Note: figures are most recent available and include both public and private long-term care expenditure.

The countries that provide genuinely adequate care — where the system does not depend on consuming the savings of careful families, where care workers are paid a living wage, where unpaid carers receive proper support — spend between two and a half and three times what the UK spends as a share of GDP.

They fund this through taxation. Denmark’s total tax burden is approximately 46% of GDP. Sweden’s 42%. The Netherlands 39%. The UK’s 36-37% sits below all of them.

The connection is not coincidental. You get what you pay for. Collectively. And the countries that pay more do not appear to be suffering the civilisational collapse that the anti-tax argument predicts. They have higher life satisfaction, lower inequality, better health outcomes and — not irrelevant to this discussion — better care systems. The trade-off between taxation and quality of life that the dominant ideology insists is inevitable turns out, on the evidence, to be largely a myth.

The Europe basket case claim — a reliable staple of British right-wing commentary — deserves a direct response. It rests primarily on the Eurozone sovereign debt crisis of 2010-2015, which was a real crisis but one rooted in the specific design flaw of monetary union without fiscal union rather than in welfare state generosity. The countries consistently cited as models for adequate care provision — Denmark, Sweden, the Netherlands, Norway — are not basket cases. They are richer than the UK in GDP per capita terms, more productive per hour worked, healthier, more equal and governed by institutions in which their citizens have considerably more trust. They achieve this while taxing more and spending more on collective provision. The connection is not coincidental. The claim that the UK cannot afford what Denmark affords is not an economic argument. It is a political choice dressed as an arithmetic constraint.

The honest political conversation is not about whether we can afford adequate care. It is about whether we are willing to pay for it. Those are different questions. The first is technical. The second is about values. And the values conversation is the one that neither the right nor the left has been willing to have honestly — because both have calculated that their voters want the provision without the bill.

At some point the bill arrives regardless. The only question is who pays it and how.

Part Six: The Contradictions Named Honestly

Before we get to the thought experiment that clarifies the values underneath all of this, the main personal objections deserve direct engagement. Each contains a real grievance. Each also contains a partial misdiagnosis.

I paid my stamp all my life. Why should my savings pay for this?

This is the most emotionally powerful objection and the one that contains the most important misunderstanding. National Insurance was never a savings scheme. It does not accumulate a personal pot. It was always a social insurance system — you paid in when you were well and working, others paid in when you needed support, and the system pooled the risk across the whole population.

The expectation of a savings-like return on a tax-like contribution was always a political fiction, maintained because it made the system politically popular and obscured the redistributive nature of what was actually happening. This does not mean the grievance is illegitimate. The system made an implicit promise — contribute throughout your working life and you will be supported in old age — and it is now struggling to honour that promise. The anger is understandable. The conclusion — that it is somehow unjust for assets to contribute to care costs — does not follow. The person with £200,000 in assets is better placed to contribute to their care costs than the person with none. What is wrong is not the principle of means-testing but the threshold — frozen at a level that catches the careful and the merely comfortable alongside the genuinely wealthy.

Why does the person who didn’t save get care when I’m paying for mine?

This objection assumes that low assets at the point of needing care reflect a failure to save rather than a lifetime of low earnings, or caring responsibilities that prevented paid work, or renting in a system that makes asset accumulation impossible, or simply bad luck. The evidence does not support the fecklessness assumption. Most people with few assets in old age were not imprudent. They were in circumstances that made prudence impossible or insufficient. The framing of deserving versus undeserving old age is the same framing applied to poverty generally and it is equally dishonest applied here.

I believe in the NHS and the state pension but not in paying more tax.

This is the central contradiction of British political culture and it deserves to be named plainly. The NHS costs approximately £204 billion per year. The state pension costs approximately £124 billion. Together they represent the single largest commitment of public expenditure. They are funded by taxation. If you want them at current levels — let alone at the levels that an ageing population will require — you need either higher taxes, lower spending elsewhere, or higher borrowing. There is no fourth option. The ideology that opposes higher taxation while defending the NHS and the state pension is not a coherent position. It is a deferral — a hope that growth will fill the gap, that efficiency savings will be found. Three decades of evidence suggests they will not.

The rich get care while I pay for it.

This contains something real. Private healthcare and private care provision do allow those with resources to access better facilities and more personalised attention. This is a genuine injustice. The answer is not to reduce collective provision but to improve it sufficiently that the private alternative loses its appeal. Which requires the fiscal commitment that this objection is often used to resist.

A footnote on a related problem at the other end of the age distribution. Approximately one in eight 18-24 year olds in the UK is currently not in employment, education or training. A significant proportion of young adults are financially dependent on parents well into their twenties. The demographic arithmetic that is supposed to fund care for the elderly assumes a working-age population that is contributing economically. If a growing share of that population cannot find secure employment or affordable housing, the dependency ratio problem is worse than the headline figures suggest. The intergenerational equity argument runs in both directions. We are asking young people to fund the care of the elderly at the same time as we are failing to provide them with the conditions that would make that contribution sustainable. This deserves its own essay. For now it is noted as a complication the arithmetic cannot ignore.

Part Seven: The Thought Experiment

Before the policy discussion — a provocation. Not a proposal. A deliberate discomfort designed to make the values underneath the arithmetic visible.

Everyone dies at seventy. The technology to enforce this exists — a mechanism at birth, a process at the limit that is painless and certain. The state’s obligation ends. The question of what to do with the elderly, the expensive, the dependent is resolved by removing them.

Take a moment with that. Notice your response.

The first response is usually outrage at the injustice. Not everyone reaches seventy. Some people are seriously ill at fifty, disabled at thirty, dead at forty-two through no fault of their own. Children lose parents too young. People at the peak of their creative or intellectual powers are removed arbitrarily. This is correct. And notice precisely what the objection reveals — you are not objecting to the principle of collective obligation. You are objecting to the arbitrariness of the cut-off. You believe society owes people something across the arc of a life. You are objecting to the specific and brutal way this version distributes that debt.

Good. Now apply the same scrutiny to the current system’s arbitrary cut-offs. The £23,250 threshold, frozen since 2010 while assets inflated around it. The postcode lottery that means identical needs produce radically different provision depending on where you happen to live. The NI contributions record that determines pension entitlement in ways that penalise interrupted working lives — which disproportionately means women’s working lives. These cut-offs are less dramatic than the seventy year limit. They are not less arbitrary. They are not less unjust in their distribution. They are simply less visible, which is why they persist.

The second response is that the wealthy will escape it. They always do. Also correct. And this reveals something too — you already know that formal equality conceals substantive inequality. The billionaire who has himself cryogenically preserved, or retreats to a jurisdiction where the rule does not apply, or simply buys his way around it — this is not a hypothetical. It is a description of how the current system already works. The billionaire gets whatever care he wants regardless of any means test. The person with £22,000 in savings gets council provision at a rate the council negotiates with the cheapest available provider. The person with £250,000 spends it down to the threshold. Formal equality. Dramatically unequal outcomes. At least the provocation is honest about its brutality.

The third response, if you get there — the one that reaches the real question — is: but I paid my taxes and my National Insurance all my life. I contributed. I am owed something in return. To which the essay has already responded above in the stamp all my life section. But the provocation sharpens it. Would you accept the seventy year limit if it came with a genuine guarantee — rigorously funded, independently verified, actually delivered — that the state would provide excellent care, free at the point of need, until that limit? Some people, on reflection, would. Not because they endorse it. Because the existing alternative — the means-tested postcode lottery of underfunded provision staffed by people paid at the tenth income percentile — is itself a form of abandonment, just a slower and more dishonest one.

To repeat this is a provocation. There is an unbreakable ethical argument which plainly tops this. But what this does reveal is that the objection to the current arrangement is not only about principle. It is about trust. Trust that the state will actually deliver what it promises in return for the fiscal contribution it demands. That trust has been eroded by decades of under-investment, frozen thresholds, broken promises and deferred green papers. Rebuilding it requires not just more money but demonstrated, sustained, visible improvement in what the money actually produces. Which is a political problem as much as a fiscal one.

Part Eight: Behind the Veil

John Rawls was an American philosopher whose 1971 work A Theory of Justice remains one of the most influential works of political philosophy of the twentieth century. His central contribution to thinking about social justice is a thought experiment he called the veil of ignorance.

Imagine you are designing the basic structure of society from scratch — its institutions, its rules, its distribution of rights and resources and obligations. You are behind a veil of ignorance. You do not know what position you will occupy in the society you are designing. You do not know your class, your gender, your race, your natural abilities, your health, your family circumstances or the length of your life. You know general facts about how economies and societies work. But you do not know where you will land.

Rawls argued that rational people designing from behind this veil would choose principles that protect the worst-off position — because any of them might end up there. Not out of altruism. Not out of ideology. Out of rational self-interest under genuine uncertainty. You would not design a system that catastrophically failed the people at the bottom if you did not know whether you would be at the bottom.

This is not the same as saying everyone should be equal. Rawls explicitly allowed inequalities — but only those that benefit the least advantaged members of society. The test for any social arrangement is not whether it makes the aggregate better off but whether it is acceptable to those who receive the least from it.

Applied to care — you do not know which position you will occupy. You do not know if you will need care at fifty-three after a stroke, or stay sharp and mobile until ninety-two. You do not know if you will be the unpaid carer sacrificing your career and your health to look after a parent, or the person whose children live abroad and cannot help. You do not know if you will be the care worker on £12 an hour doing the most important work in the building, or the person whose fees pay that care worker’s wage, or the fund manager whose financial model extracts margin from the care home chain. You do not know if you will accumulate assets through a rising housing market you did nothing to create, or rent all your life and arrive at old age with nothing.

Design the system from behind that veil.

Almost everyone, genuinely engaging with this thought experiment, arrives at something like: I would want a system that provides decent care regardless of accumulated assets, funds it through taxation proportionate to income and wealth, values care work adequately, and supports unpaid carers without destroying their financial security and health in the process.

This is a description of what the Nordic countries have built. At a fiscal cost — tax as a share of GDP — that British political culture has consistently refused to pay while demanding comparable outcomes.

The veil does not resolve the dilemma. It clarifies it. The question is not whether we should have collective provision. Almost everyone behind the veil chooses collective provision. The question is whether we are willing to be honest about what it costs and who should pay for it. And that is a question about political courage rather than philosophical principle.

Part Nine: The Bottled Politics

Every government since at least 2010 has known broadly what needs to be done. None has done it.

The Dilnot Report of 2011 — commissioned by the Coalition government, produced by Andrew Dilnot with rigour and clarity — proposed a lifetime cap on care costs and a significantly raised means-test threshold. It was a serious response to a serious problem. It gathered dust for a decade while the problem worsened.

Theresa May‘s 2017 manifesto proposed what the press immediately and fatally dubbed the dementia tax — a system that would have included the value of people’s homes in the means test for domiciliary care. The policy was not obviously wrong in principle. It addressed a genuine anomaly — care home residents had their homes counted in the means test while people receiving care at home did not, creating a perverse incentive to enter residential care unnecessarily. But it was presented without a cap, appeared to penalise people for staying in their own homes, and was partially reversed within days in one of the most politically damaging U-turns in recent electoral history. The phrase nothing has changed became the defining image of May’s premiership. The policy’s collapse set back serious care reform by years — demonstrating with brutal clarity the political toxicity of any proposal that appeared to threaten the family home, however justified in principle.

Boris Johnson stood on the steps of Downing Street in July 2019 — his first statement as Prime Minister — and promised he had a clear plan to fix the social care crisis once and for all. The plan, when it eventually emerged in 2021, was a lifetime cap set at £86,000. This was higher than Dilnot had recommended and — crucially — applied only to care costs rather than to the daily living costs in residential care such as accommodation and food, meaning most people would reach the cap far later than they expected, if at all. The reform was scheduled for implementation in 2023, delayed to 2025, and then scrapped entirely by the incoming Labour government in July 2024 on grounds of fiscal cost. The promise made on the steps of Downing Street was never delivered. The clear plan did not exist in the form implied.

Labour. The current government almost certainly has a view on what needs to be done. It has not shared it in a form that commits to a funding mechanism. The word reform appears regularly. The word funding does not follow it with sufficient specificity to mean anything. This is not unique to Labour — it is the consistent behaviour of governments that understand the problem and calculate that the political cost of honesty about the solution exceeds the political cost of continued deferral.

A word here about the bond markets — because any serious proposal to increase public expenditure on care, pensions and healthcare by the amounts required to match Nordic provision will be scrutinised by them before it is judged by the electorate. The Liz Truss episode of 2022 is the cleanest available demonstration of what happens when a government announces significant fiscal commitments without a credible funding plan — the gilt market responded before the electorate did, and the response was immediate, brutal and politically terminal. Any serious care reform package has to come with a detailed, independently assessed and fiscally credible plan. Not because the bond markets are always right — they are not — but because their confidence is a precondition for the borrowing costs that make any long-term investment affordable. Telling the bond markets that you intend to raise taxes to fund care is not political weakness. It is the precondition for being taken seriously about doing it. The absence of a credible fiscal plan is not prudence. It is deferral dressed as caution.

The Association of Directors of Adult Social Services has estimated there remains a funding gap of over £1 billion for adult social care simply to stand still next year. Standing still is not the ambition. Standing still is not being achieved.

The structural problem is compounded by an institutional one that rarely receives the attention it deserves. Adult social care in England is not a national service like the NHS. It is a local government responsibility — funded primarily through council tax and central government grants, commissioned by 153 separate local authorities, each with its own eligibility criteria, fee rates and provision models. The postcode lottery is not an accident of implementation. It is built into the architecture.

This matters because the finances of English local government were already in serious difficulty before the care crisis reached its current severity. A decade of austerity from 2010 reduced core central government funding to local authorities by approximately 40% in real terms. Councils responded by cutting discretionary services — libraries, leisure centres, youth provision, road maintenance — to protect their statutory obligations, of which adult social care is the largest. By the mid-2020s several councils had issued Section 114 notices — the local government equivalent of insolvency — and many more were operating on reserves that gave them months rather than years of headroom.

The result is a care system that is simultaneously a national crisis and a local responsibility, funded through a mechanism — council tax — that is regressive, geographically uneven and structurally incapable of raising the amounts required. Areas with the highest care needs — older, poorer, more rural populations — tend to have the lowest council tax bases. The gap between need and resource is widest precisely where the problem is most acute. Central government top-up grants help at the margin. They do not resolve the structural mismatch between a national demographic challenge and a local funding mechanism.

Any serious reform of care funding therefore requires not just more money in aggregate but a fundamental rethinking of how the responsibility for care is distributed between national and local government — and who bears the fiscal risk when demand outstrips provision. The current arrangement gives local authorities the obligation without the resources to meet it, and then points at local failure when the inevitable consequences emerge. This is not a design flaw. It is a design feature. It allows central government to set the promise and localise the blame.

Part Ten: The Honest Statement of What Is Required

Not a programme. A direction.

Adequate collective provision of care, pensions and healthcare for an ageing population requires a sustained increase in public expenditure as a share of GDP. The magnitude is debatable. The direction is not. The OECD data is unambiguous — the countries that provide genuinely adequate care spend more and raise more in tax.

The fiscal options are not unlimited but they are not as constrained as the political conversation suggests. A wealth tax on assets above a defined threshold — including housing equity above a reasonable level — would raise substantial revenue from those who have benefited most from the asset price inflation of the past thirty years and who did nothing to create that inflation. A land value tax would capture unearned gains from rising land values. A genuine reform of National Insurance to remove the ceiling above which high earners stop contributing would raise significant revenue from those most able to provide it. A serious inheritance tax — rather than the current system honeycombed with exemptions — would address the specific injustice of care costs consuming assets that families had planned to pass on, by treating those assets as a collective rather than purely private resource.

None of these are technically complicated. All of them are politically difficult. The difficulty is the point.

We have elsewhere in this series sketched a longer-term proposal — the commons equity fund, drawing on mandatory equity issuance from major technology and financial companies as correct initial distribution of the returns from collectively created value. Scoping that fully is for another essay. But it is worth noting here that a 1% annual equity issuance requirement on the global technology sector alone — at the lower end of what these companies routinely issue to their own employees — would at current valuations transfer several hundred billion dollars annually into public hands. The funding problem is not fundamentally one of arithmetic. It is one of political will and institutional design.

The alternative to political will is the current arrangement — continued deferral, salami-sliced provision, the invisible subsidy of unpaid carers, the self-funder trap consuming the savings of careful families, the care worker on £12 an hour, and the green paper that is always being written and never quite published.

At some point the deferral ends. The question is whether it ends through honest collective choice or through the kind of crisis that removes the choice entirely.

The arithmetic does not get more favourable with time. The demographic curve does not flatten. The unpaid carers are not getting younger. The care workers are not staying in jobs that pay them at the tenth income percentile.

This is a choice. It is being made continuously, in the decision not to decide, by governments that know what they are doing and calculate that the political cost of honesty exceeds the political cost of deferral.

They may be right about the politics. They are wrong about the arithmetic.

And now a final provocation. In an unpredictable, multi-party miasma, where rage and disappointment have replaced loyalty and habit, they may not even be right about the politics. They can be cautious and still lose. They can defer and still be punished. The guaranteed outcome of doing nothing with power is the reputation for having wasted it. They are near certain to lose as the pendulum swings back to the other side. So why not grasp the nettle. You have nothing further to lose and everything to gain. The amelioration of actual harm to actual people, plus eschewing the compounding arithmetic that makes the eventual reckoning worse. The asymmetry favours action.

And a final, final provocation. If you are reading this you might be thinking that I am saying you will have to pay more tax, now or in the future. So, for clarity, I am saying you should pay more tax. Pretty much all of you. 5% on income tax bands and 0.5% on wealth p.a. above £1m. Back of the envelope £70-80bn. That will take care of the above.

Next: Essay Six B — The Work of Love. Who does this work, what it actually involves, what its devaluation costs everyone, and what a care economy organised around dignity would look like.

The manifesto these essays argue toward — Listen to Me — is on this blog. The gaps in these arguments are real and acknowledged. If you see them, say so. The conversation is the point.

Leave a comment